We can help you navigate protecting your home, car, or business.

HOME INSURANCE

Home Insurance in Texas

Home is where the heart is for all of us, so your home is worth protecting! At Marek Insurance,

we help you tailor a homeowner plan that fits your needs.

What is Home Insurance?

In basic terms, homeowners insurance will protect you in the event a disaster or an accident affects your home. It will cover the structure itself (your house) along with what’s inside (your belongings).

When it comes to what can be covered, the spectrum is really quite broad. Homeowners insurance can protect you in the case of storms, fallen trees, or others. It covers your loss from burglary and is even your personal liability protection if someone is injured on your property.

Why Get Home Insurance?

Your home is your happy place, your safe space making it your most valuable possession. From raising a family to simply relaxing at the end of a long hard day, it’s the one place you probably couldn’t live without. It’s also important to cover everything inside your property, from high-tech gadgets to sentimental jewelry, which can be just as important

Is Home Insurance Legally Required in Texas?

In most cases, obtaining home insurance is not legally required in Texas, but you might be contractually obligated to get homeowners insurance by your mortgage provider or condo association.

Generally, having home insurance coverage is highly recommended to help you recover should the worst occur.

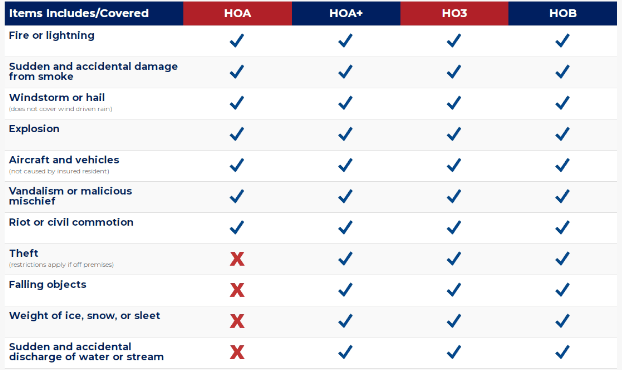

What Are the Different Policy Types?

What Are the Different Policy Types?

What Are the Different Policy Types?

What Are the Different Policy Types?Homeowner insurance is most often secured on one of the following types of policy forms:

- HOA

(Named Perils)

This is the most basic policy, and coverage includes protection for specific ‘named perils’ such as fire and vandalism. It only covers items that are specifically named. If the type of claim is not named, the claim will not be covered.

- HOA+

(Expanded version of the HOA)

This expanded policy covers everything in the HOA basic plan unless specifically excluded, plus additional Named Perils.

- HO3

(National Form Open Peril)

This is the most frequently purchased homeowner insurance policy. It provides broader coverage for various types of losses that can cause damages to your home/possessions and includes personal liability coverage. There are fewer exclusions than the HOA+ policy and the coverage amounts are higher for certain items.

- HOB

(Texas Form Open Peril)

This HOB is similar to the HO3 policy; they provide coverage for your home on an Open Perils bases, but the HOB also provides additional water damage protection.

How Much is Home Insurance In Texas?

The cost of a homeowner insurance policy largely depends on the year built, age of the roof, type of roof, location of the property, deductibles, proximity to the coast, and applicable discounts. The cost of homeowner insurance may not be as high as you may think; however, Texas does have slightly higher rates than other states due to increased weather damage risks.

Best Ways to Save on Homeowners Insurance

There are many ways you can save on homeowner insurance; our agents can offer professional advice and shop over forty home insurance carriers to secure coverage that fits your needs. Family

Family-owned and operated Marek Insurance Agency has a long-standing reputation for providing a trusted, tailored service. Family-owned and operated, Marek Insurance Agency has a long-standing reputation for providing trusted, tailored insurance services.

We have been serving homeowners in Crosby and the surrounding area for almost 40 years:

- Crosby

- Atascocita

- Baytown

- Dayton

- Deer Park

- Highlands

- Huffman

- Humble

- Kingwood

- Mont Belvieu

- Pasadena

- South East Houston

Ready to Benefit From Decades of Expertise?

Get in touch with Marek Insurance today, and one of our experienced agents will assist you with honest, knowledgeable advice and a range of policy options. Unlike other insurance providers, we have access to a vast network of insurance companies to find a plan that fits your needs.